America's Other Great Depression

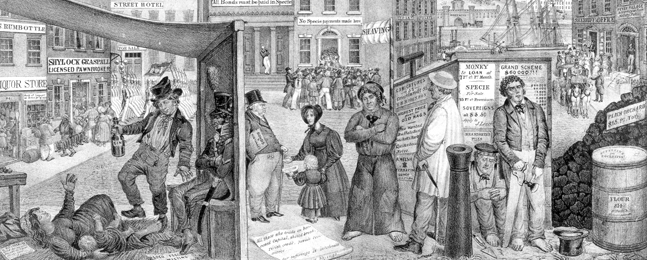

DOWN AND OUT: A fanciful street scene in New York depicts the effects of the financial panic of 1837 — especially on the working class.

by Michael Hardy

It was a time of rapid economic growth, fueled by easy credit and rampant speculation in Western land that drove prices into the stratosphere. Just as quickly, the bubble in land prices burst, leading to a nationwide run on the banks. Lacking enough gold and silver in their vaults to redeem for paper money, banks either declared bankruptcy or temporarily shut down. Sound familiar?

The Panic of 1837, America’s worst financial crisis of the 19th century, shares sobering parallels with the financial crash of 2008, says Jessica Lepler, PhD’08. Like the more recent crisis, the 1837 panic had disastrous effects. Between 1837-42, total bank assets fell by almost half, credit dried up and business slowed to a crawl. Annual growth in per capita investment dropped from an estimated average of 6.6 percent in the five years before the crash to -1.0 percent in the five subsequent years. In the midst of the crisis, the British ambassador to the United States reported to London that “it would be difficult to describe, or render intelligible in Europe, the stunning effect which this sudden overthrow of commercial credit and honor of the nation has caused.”

In September 2008, just as Lepler was starting a new job as assistant professor of history at the University of New Hampshire, Lehman Brothers collapsed, sending the stock market plummeting, destroying trillions of dollars in value and plunging the country into what has become known as the Great Recession. Suddenly, everyone was interested in financial crises, including Cambridge University Press, which later this year will publish “The Many Panics of 1837,” a book version of Lepler’s Brandeis dissertation.

Early in her graduate studies, Lepler had planned to study early-20th-century Jewish women intellectuals, the subject of her senior thesis at Tulane. But she quickly found herself gravitating toward economic history, especially the nascent subfield of “failure studies,” which focuses on the victims of American capitalism rather than its success stories.

“Nobody could understand why I picked this topic,” she says. “First of all, I’m not an economic historian, so how am I going to write about this without having the quantitative and theoretical background? Second, why in the world would I be interested in something like a financial crisis? People told me it was depressing.”

Mike Lovett

Jessica Lepler, PhD'08

page 2 of 3

Lepler chose to focus on the cultural history of the 1837 crisis rather than its economic implications. “From the beginning, I was less interested in the question of cause and more interested in how ideas about causation came to be formed,” she says. “What actually made people panic, and what did it mean to panic? What I discovered many years later is that there were many panics in 1837. There were individual panics, and there were local panics. Even the term ‘Panic of 1837’ has many different meanings, because every scholar has defined it in her own way.”

Lepler’s dissertation director, Jane Kamensky, the Harry S. Truman Professor of American Civilization, is the author of the award-winning 2008 book “The Exchange Artist,” centered on the 1809 collapse of the Boston Exchange Coffee House, one of America’s first bank failures. “She didn’t have to persuade me that she’d chosen an important topic,” says Kamensky. Lepler’s painstaking archival work resulted in what Kamensky calls “a masterly dissertation.” In 2008, Lepler won the prestigious Allan Nevins Prize for the nation’s best-written dissertation on an American subject, the second of three Brandeis PhDs to win the prize since 2005.

Attention to detail distinguishes Lepler’s work from other histories of the 1837 crisis, says Kamensky: “She was incredibly dedicated to finding out how the processes of 19th-century finance really worked. This was a world before faxes, before telegraphs, before regular steamships, when the sharing of information over distances was itself a major hurdle. Jessica worked in really novel ways to figure out just how people got credit extended for them, for example, and how they negotiated not only over time but over space. What would you know about London in New Orleans when you had to make a decision about selling your cotton? Or what would you know in London when you had to make a decision about granting someone a loan?”

Since books about finance are often dominated by stories of wealthy bankers and powerful politicians, Lepler made a special effort to include other perspectives in her narrative of the panic. While working in the Bank of England (BOE) archives, she stumbled upon the record of an internal investigation the BOE conducted in 1836 of a junior clerk named Thomas Fidoe Ormes. Ormes, whose father, grandfather and great-grandfather had also worked at the BOE, had heard a rumor that George Wildes & Co., a major mercantile house, was on the verge of collapse. He unwisely confided the secret to a stockbroker friend, who betrayed Ormes’ trust by spreading the information all over London.

By that evening, speculation about the house’s imminent failure filled the newspapers. BOE officials discovered that Ormes had learned about the rumor from a blind clerk, who had overheard a deaf clerk’s message. From such trivial gossip are financial crises made.

“It’s the stuff of novels. I call it the case of the leaky clerk, because Ormes was on his way to the toilet when he leaked the rumor,” says Lepler, laughing. “It’s so rare when you study business history to discover the voices of the people who weren’t in charge.” Ormes’ story is typical of Lepler’s social-historical “bottom-up” approach to the Panic of 1837.

When Lehman Brothers declared bankruptcy in 2008, Lepler was busy turning her dissertation into a book. As a historian, Lepler didn’t want current events to contaminate her research on the 19th century, so she tried to avoid reading newspapers or watching television, relying upon her boyfriend to keep her updated. But she couldn’t help being fascinated by the language headline writers used to describe what was occurring.

“They used the same metaphors as the people I was writing about,” Lepler says. “They called it a tornado, an illness, an earthquake — all these natural-world metaphors.” Just as in 1837, Americans were looking for a scapegoat. “The most interesting parallel for me has been watching the stories of blame. How do we construct the narrative of our financial crisis — who gets blamed? Who are the evildoers, and whose fault is it?”

page 3 of 3

Lepler was less surprised than most Americans by the events of 2008. Since the late 18th century, the American economy has experienced minor crises approximately every 10 years and major calamities every 20. Before 2008, the last stock market crash was the savings and loan collapse of 1987, which meant that America was due for a shock. (The dot-com meltdown of 2000 occurred almost exactly halfway between the two crises, as could have been predicted.)

Why do financial crises occur at such regular intervals? Lepler believes the answer lies in human psychology. “Financial crises are really shocking events,” she says. “They’re incredibly scary, and they force people to rebuild their lives. It takes time to do that rebuilding. And after people regain faith, the country usually experiences a decade of prosperity. Then you have that period before the crash when people experience a kind of mania. And then you get another crash.”

Lepler predicts it will take about seven years for America to fully recover from the 2008 crash, which, if true, means that the economy should get its mojo back around 2015. If history repeats itself, the country will then enter a period of explosive growth, interrupted by a small crash in 2018 and terminated by a bigger one in 2028.

Of course, not everyone suffers in a panic. Among the people Lepler studied were the minority of investors who, like the short-sellers Michael Lewis recently profiled in his best-selling book “The Big Short,” got rich while so many others went broke. In a way, Lepler identifies with these much-loathed individuals.

“When I was in graduate school, questions of the economy were far from mainstream,” she says. “When I was writing the dissertation, I used to call some of the people I was studying ‘panic profiteers’ because their careers were built out of the panic. Now I say that I’m the last panic profiteer.”

Michael Hardy is the arts editor of Houstonia magazine.